Python是進行數據分析的一種出色語言,主要是因為以數據為中心的python軟件包具有奇妙的生態係統。 Pandas是其中的一種,使導入和分析數據更加容易。

Pandas dataframe.resample()函數主要用於時間序列數據。

時間序列是按時間順序索引(或列出或繪製圖形)的一係列數據點。最常見的是,時間序列是在連續的等間隔時間點上獲取的序列。這是用於頻率轉換和時間序列重采樣的便捷方法。對象必須具有datetime-like索引(DatetimeIndex,PeriodIndex或TimedeltaIndex),或將datetime-like值傳遞給on或level關鍵字。

用法: DataFrame.resample(rule, how=None, axis=0, fill_method=None, closed=None, label=None, convention=’start’, kind=None, loffset=None, limit=None, base=0, on=None, level=None)

參數:

rule:表示目標轉換的偏移量字符串或對象

axis:int,可選,默認0

closed:{'右左'}

label:{'右左'}

convention:僅對於PeriodIndex,控製使用規則的開始還是結束

loffset:調整重新采樣的時間標簽

base:對於平均細分為1天的頻率,請使用匯總間隔的“origin”。例如,對於“ 5分鍾”頻率,基本範圍可以是0到4。默認值為0。

on:對於DataFrame,使用列而不是索引進行重采樣。列必須為datetime-like。

level:對於MultiIndex,用於重采樣的級別(名稱或數字)。級別必須為datetime-like。

重新采樣會根據實際數據生成唯一的采樣分布。我們可以應用各種頻率來重新采樣我們的時間序列數據。這是分析領域中非常重要的技術。

最常用的時間序列頻率是-

W:每周頻率

M:月末頻率

SM:半月結束頻率(15日和月末)

問:四分之一結束頻率

有許多其他類型的時間序列頻率可用。讓我們看看如何將這些時間序列頻率應用於數據並對其重新采樣。

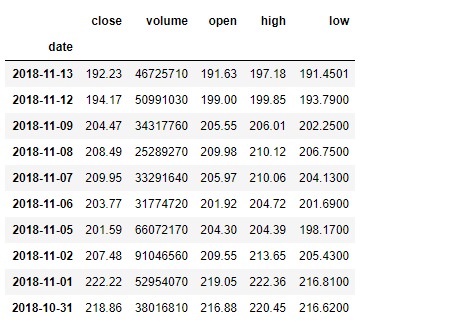

有關在代碼中使用的CSV文件的鏈接,請單擊此處

這是蘋果從(13-11-17)到(13-11-18)持續1年的股價數據

範例1:按月頻率重新采樣數據

# importing pandas as pd

import pandas as pd

# By default the "date" column was in string format,

# we need to convert it into date-time format

# parse_dates =["date"], converts the "date"

# column to date-time format. We know that

# resampling works with time-series data only

# so convert "date" column to index

# index_col ="date", makes "date" column, the index of the data frame

df = pd.read_csv("apple.csv", parse_dates =["date"], index_col ="date")

# Printing the first 10 rows of dataframe

df[:10]

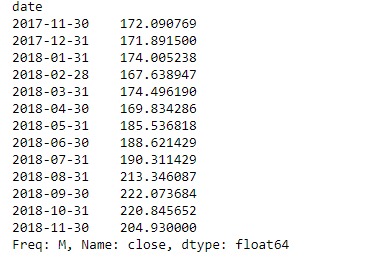

# Resampling the time series data based on months

# we apply it on stock close price

# 'M' indicates month

monthly_resampled_data = df.close.resample('M').mean()

# the above command will find the mean closing price

# of each month for a duration of 12 months.

monthly_resampled_data輸出:

範例2:按周頻率重新采樣數據

# importing pandas as pd

import pandas as pd

# We know that resampling works with time-series data

# only so convert "date" column to index

# index_col ="date", makes "date" column.

df = pd.read_csv("apple.csv", parse_dates =["date"], index_col ="date")

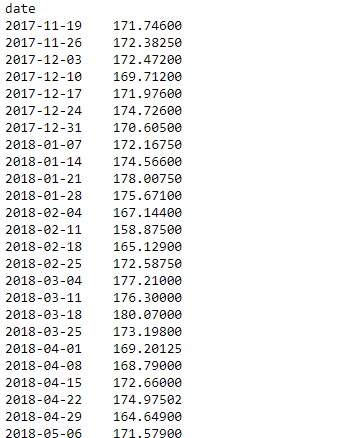

# Resampling the time series data based on weekly frequency

# we apply it on stock open price 'W' indicates week

weekly_resampled_data = df.open.resample('W').mean()

# find the mean opening price of each week

# for each week over a period of 1 year.

weekly_resampled_data輸出:

範例3:按季度頻率重新采樣數據

# importing pandas as pd

import pandas as pd

# We know that resampling works with time-series

# data only so convert our "date" column to index

# index_col ="date", makes "date" column

df = pd.read_csv("apple.csv", parse_dates =["date"], index_col ="date")

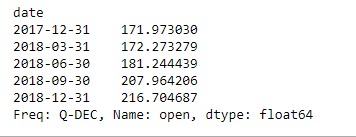

# Resampling the time series data

# based on Quarterly frequency

# 'Q' indicates quarter

Quarterly_resampled_data = df.open.resample('Q').mean()

# mean opening price of each quarter

# over a period of 1 year.

Quarterly_resampled_data輸出:

相關用法

- Python pandas.map()用法及代碼示例

- Python Pandas Series.str.len()用法及代碼示例

- Python Pandas.factorize()用法及代碼示例

- Python Pandas TimedeltaIndex.name用法及代碼示例

- Python Pandas dataframe.ne()用法及代碼示例

- Python Pandas Series.between()用法及代碼示例

- Python Pandas DataFrame.where()用法及代碼示例

- Python Pandas Series.add()用法及代碼示例

- Python Pandas.pivot_table()用法及代碼示例

- Python Pandas Series.mod()用法及代碼示例

- Python Pandas Dataframe.at[ ]用法及代碼示例

- Python Pandas Dataframe.iat[ ]用法及代碼示例

- Python Pandas.pivot()用法及代碼示例

- Python Pandas dataframe.mul()用法及代碼示例

- Python Pandas.melt()用法及代碼示例

注:本文由純淨天空篩選整理自Shubham__Ranjan大神的英文原創作品 Python | Pandas dataframe.resample()。非經特殊聲明,原始代碼版權歸原作者所有,本譯文未經允許或授權,請勿轉載或複製。